[ad_1]

Financial illiteracy is a cardinal issue within societies. By using the Socratic method, we can ask questions that get to the root of the issue.

Most, if not all, individuals are provisioned with zero financial education and are not given sufficient instruction in the first principles of money, especially as it relates to building wealth and establishing a secure foundation from which to operate so that they may most optimally navigate the challenges of life.

Financial education is entirely omitted in classrooms, students are not furnished with the necessary faculties to effectively contend with the realities of existence and this is not solely limited to financial education either. Other notable curricular deletions include a lack of effective tutoring surrounding nutrition, physical education, self-defense, effective communication and negotiation skills, mental resilience, etc. To the more perspicacious among us, this has always been evident.

Indeed, many are aware that the opposite is typically the case: teenagers are encouraged to take on colossal amounts of debt to secure a university education, condemning them to the Sisyphean trial of endeavoring to pay back their debts while simultaneously facing minimal prospects of employment. Beyond this, many are encouraged to build their credit score by shouldering increasing amounts of debt, taking on death pledges (mortgages) and living life above their means — with this lifestyle being considered “normal” for most in the Western world and across the globe.

We are constantly being handed advice from individuals who have no experience in building wealth. Parents, teachers, friends and even media pundits, although seemingly well-intentioned, in reality live paycheck to paycheck and have no concrete understanding of the handling of money or lack the ability to competently allocate their capital in order to ensure its sanctity.

Sit Down And Shut Up

The following personal anecdote illustrates this problem quite nicely.

As a boy, I was once reprimanded by a school teacher when he elucidated the class about how the world ”really works,” extolling the alleged virtues of “getting a good education, working hard, saving money” and proffering advice surrounding the merits of pursuing a career. Having identified a singular glaring hole in his arguments, I quipped: “Sir, why would I take advice from somebody who has never left school?”

Needless to say, I spent the next hour outside the classroom in the hallway to “think about what I had said.” Indeed, to this day I still think about that interaction and the validity of the retort seems to become more and more apparent as time goes on. In my mind, I was merely employing the Socratic method to better understand my teacher’s inadequacy to proliferate his advice to the class.

My teacher’s response is emblematic of the attitude adopted by most individuals in society today, acceptance of the status quo and overreliance on outdated models of operating in the world — which are increasingly becoming more and more anachronistic, particularly as they relate to one’s finances and future prospects. If anything challenges that long-held assumption, it is quickly ridiculed or punished.

To be clear, endeavoring to attain a good education and working hard are indeed virtuous, worthwhile pursuits, but the means for acquiring these things or enacting them are multi-dimensional. The world is rapidly changing and the digital universe is offering opportunities that never existed before, serving to disrupt the monopoly that legacy systems have enjoyed for centuries past.

Faith in our existing institutions has all but evaporated, owed primarily to their lack of leadership and their cascade into corruption; with the odor of lies and deceit filling the halls of our establishments, their repugnant behavior is apparent to all. The existing paradigm serves to solely usufruct and usurp our time, energy and value.

As such, this article addresses these matters and provides an explanation as to why Bitcoin is the remedy and lighthouse in the fog. It details the most common proclamations concerning bitcoin’s supposed instability and purported unsuitability as a viable and secure means for storing one’s wealth, as well as presenting its virtues in three major domains which facilitate its claim as the safest place for one’s money — namely how bitcoin satisfies the functions of security, integrity and transportability.

- Integrity: Integrity refers to an asset’s anti-fragility and resiliency against corruption of the protocol. The protocol being the safeguarding and fortification of your monetary energy.

- Security: Security refers to its resiliency to external hostile attack vectors.

- Transportability: Referring to the ability with which one can physically transport one’s wealth across geopolitical domains as well as the facility with which one can readily transact with other market participants with minimal impedance or friction, i.e., ease of transactability/liquidity.

Asking Questions

A valuable lesson was learned when I asked my teacher that question: the importance of challenging authority figures and their biases, identifying illogical fallacies in one’s arguments and the importance of asking the “why” of things.

Therefore, before we survey each distinct aspect of bitcoin’s supremacy as the safest means for storing one’s wealth, we should begin by prefacing this matter with a brief discussion surrounding the concept of saving itself and its relevance to our lives.

Employing a first principles approach to money management will allow us to better understand the necessity for appropriately allocating our capital in order to improve our financial health and attain prosperity. Therefore, let us begin by employing a Socratic approach which will allow us to better comprehend why it is necessary to store our wealth in bitcoin.

Saving For A Rainy Day

The concept of saving is repeatedly parroted by mainstream society and financial “experts” and has served to become axiomatic in the minds of many. “Save your money for a rainy day” is a mantra that is embedded into the psyche from a young age. However, we do not pause to ask two fundamental questions in response to those assertions:

1) What is it we are “saving?”

2) Where do we “save” it?

Therefore, allow us to investigate the matter.

In common parlance we say that we are “saving” or “building up our savings,” but what is it that we are actually saving or attempting to save? Well, our money of course, which naturally begs the preceding question of what precisely money is.

You trade time and energy to generate value to the marketplace whereby you are compensated with money which acts as a representation of your stored time, value and energy in service to that marketplace. As a natural corollary to this, in everyday vernacular, we also say that we “spend” time; we spend time with our friends and family, we spend time in meditation, we spend time doing our hobbies, etc. Money and time, then, cannot be disentangled — they are synonymous — money simply being a representation of expended time.

Big deal — what does it matter? Well, although this may appear arbitrary, it unfortunately matters a great deal , since most store their time in fiat currency, which can (and is) printed out of thin air, therefore devaluing the total existing stock. The more of something that exists the less scarce it becomes and therefore the less value it retains. With the direct opposite policy producing the polar opposite result: the scarcer the more valuable it becomes (assuming that demand remains constant). The heart of the problem is that you are exchanging the scarcest thing you possess — your time and energy — for something that has no scarcity at all, a defective money in fiat currency.

In the existing paradigm the way to combat this and insulate your purchasing power requires that the individual generate a return on their money, and that return needs to be superior to the current inflation rate — that is what the game is really all about. Before bitcoin appeared, the typical way to do this was by finding innovative ways to generate said return through various investment vehicles.

The traditional remedy to this problem is engaging in the financial markets, which means that one has to assume some element of risk in order to secure their purchasing power into the future — a system whereby individuals have to assume more and more risk to keep up with increasing levels of inflation, begetting a comprised societal foundation.

Bitcoin ameliorates this problem since it once again allows the individual to actually save their money and not need to assume the risk of investment when all they wish to do is to have some insurance against the uncertainty of the future and increase their prospects of security and stability in their lives, as we shall see.

Sound Money Versus Soft Money

This effectively comes down to the choice of holding your wealth in sound money or soft money. In order to differentiate between the two, we can look to the three pillars mentioned at the introduction of this article which guarantee the sanctity of our savings, these being its integrity, security and transportability/liquidity.

Let us now assess those three pillars and contrast the use of banks with the use of bitcoin and how well each satisfies these properties.

Bank

Integrity: Fiat money stored in a bank benefits from zero integrity because of a lack of protection from inflation since the interest rate does not beat even the official inflation rate. As a result, keeping your money in your bank account means that you are mathematically guaranteed to lose purchasing power.

Security: The security aspect of banks is somewhat better. It is hard for someone to enter a bank and steal your money; the cash is either stored behind four feet of steel in a vault or nowadays, stored digitally. However, although suitable for protecting against malicious external attacks, an individual’s bank account is another matter since the possibility of confiscation or deplatforming is always present. Counterparty risks always exist, as can be seen with recent events in Canada.

Transportability: Fiat paper money was a useful invention which allowed individuals the benefit of transacting and transporting their wealth more easily across space. However, this benefit only exists within the individual’s respective geopolitical domain. It would prove problematic if one were required to leave their country in the case of an emergency, as can be seen with the recent crisis in Ukraine.

There is no use withdrawing cash and carrying it across borders since it would be either useless in a country with a different currency or the exchange rate would prove unfavorable and thus not optimally liquid, as well as presenting a pronounced risk to one’s safety because of susceptibility to theft or coercion. Cash therefore, is not flawless in transporting one’s wealth across geopolitical domains.

Therefore, a bank is only marginally better than keeping cash under your mattress.

Bitcoin

Integrity: Bitcoin does not suffer from the corrosive effects of inflation as a result of its perfectly fixed supply. It is actually deflationary in nature with its integrity always guaranteed, since no individual or entity can alter the supply cap owing to its decentralization. There is no requirement to assume counterparty risk.

Security: If an individual takes full custody of their bitcoin (which they are encouraged to do) no individual or party can gain access to those funds if the owner holds those keys.

Transportability: Referring back to the concept of money being an insurance policy against the inherent uncertainty of the future and a means for optimizing pure optionality as a bulwark against said uncertainty, bitcoin allows an individual to store their wealth in an asset that can be moved across geopolitical domains in the confines of their very minds.

You can enter a new country with all of your wealth intact, purchase a sim card and spend your bitcoin or sell it for the local currency to purchase food and accommodation. Most people’s wealth is stored in their homes as equity, which is highly illiquid, taking around six months to transact. The money in their bank accounts may also prove useless in another country where their bank accounts may not be valid or the currency different.

The recent crisis in Ukraine effectively highlights the importance of possessing transportable wealth. The modern world is in a constant state of flux and the growing necessity for individuals to flee their inherited nation states grows by the month; bitcoin offers an unparalleled opportunity for individuals to reclaim their autonomy in a world set on minimizing or altogether eviscerating it.

Central Bank Digital Currencies

A brief point and warning should be made here concerning the upcoming implementation of Central Bank Digital Currencies (CBDCs). CBDCs are programmable digital currencies which can be manipulated by governments, central banks and employers.

Although CBDC proponents advocate for its use as means of protection against fraud and money laundering, they conveniently omit the tremendous power imbued in its issuers. CBDCs will allow the issuer to enact full control over its users’ money: customize interest rates, set expiry dates and regulate specific uses are just some of the possibilities that exist with this programmable money.

And what might be the result of this if these CBDCs can be linked to a digital ID? If your political stance is viewed as unfavorable to the establishment? What happens if you cannot purchase investments or you are given a negative interest rate because you are saving too much money and are thus incentivized to spend and consume?

Having demonstrated that allocating your capital within the confines of a bank is a liability, it is becoming increasingly apparent that entrusting your money to these institutions will no longer remain solely a liability. Fiat money and the banking system will begin to pose a significant threat not just to your financial sovereignty, but also to your individual free will. The implementation of CBDCs actually imperils an individual’s right to self-determination; it presents a very clear and present danger jeopardizing liberty, sovereignty and freedom.

Bitcoin and CBDCs are diametrically opposed. They are polar opposites in their philosophies; one grants sovereignty, the other slavery; one offers self-custody and the other, total control.

Bitcoin Is Better Than Banks

Bitcoin fortifies your money and restores the individual’s ability to save rather than purchase speculative investments. Bitcoin has no CEO; Bitcoin has no shareholder meetings; Bitcoin just is.

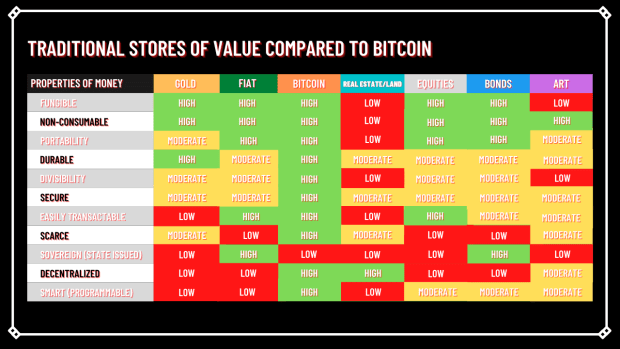

Of course, an astute reader will understand that bitcoin and banks are not the only options when it comes to allocating one’s capital. There are other investment options such as precious metals, real estate, government and corporate bonds, fine art, wine, antiques and many other options that could be used as stores of value. According to Nassim Taleb, you could even use olive oil.

However, bitcoin remains supreme in its role as the optimum store of value based on it being able to most effectively satisfy the core properties of money as demonstrated above. To further compound this point, the following image provides a matrix illustrating a side-by-side comparison of each traditional store of value juxtaposed to bitcoin.

Volatility

“Bitcoin is too volatile.”

This is a recurring mantra that is consistently perpetrated by Bitcoin’s detractors as a reason for it not being a safe bet. In my opinion, you can’t blame them since they are oftentimes simply regurgitating what is expounded by the mainstream media in order not to appear ignorant on the subject. It is an automated response, derived from hysterical headlines. Allow us to dismantle it.

We have established that bitcoin is the most secure asset available to market actors, possessing the greatest integrity and security as well as offering the best means for transportability. Where does volatility have a role to play?

Let us begin to explain what volatility is and why bitcoin is not volatile whatsoever. Let us continue in our approach of asking questions. What is it that is volatile about bitcoin precisely? The price is volatile.

The price of bitcoin is indeed volatile if you are measuring the asset in terms of fiat currency, but price does not always equate value or worth. This is why one can pontificate that an asset or object can either be considered undervalued or overvalued; consideration is based upon what one subjectively believes the asset to be worth.

Price is simply the objective current exchange rate for a particular good or service, i.e., what one is required to pay to receive its benefit; but the price itself, although objective, is determined by the subjectively perceived value of an asset’s worth and value. We all assign value to different things — some find value in collecting baseball cards, others find value in learning how to crochet, while there are others who find zero value in either of those practices and so do not engage.

The more value something has, the greater its worth, meaning that it will command a higher price, since all of these factors are interdependent. Since value is derived from demand, scarcity and perceived usefulness, which together form the foundation of bitcoin’s use case, the volatility of the price of bitcoin can easily be reconciled since it has a fixed and diminishing supply: coupled with increasing demand, it results in an ascendance in price.

You Can’t Lose Money With Bitcoin

A bold claim.

When one stops to consider the matter, they inevitably realize that they can’t lose any money. Certainly, the value of their bitcoin measured in fiat may fluctuate but their holdings have not gone anywhere. Seasoned veterans in the Bitcoin space have no interest in the fluctuations in the fiat price of bitcoin; that metric is inconsequential to them and poses no relevance because they use a different means of measurement. They have begun to denominate things, not in fiat terms but in bitcoin terms, which is why the meme “1 BTC=1 BTC” is so prevalent, since it effectively illustrates this point.

Everything is currently denominated in fiat in most people’s minds, but when one begins to shift one’s mindset and starts denominating things in bitcoin terms, and eventually in satoshis, the picture becomes much clearer. Therefore, once you begin this process and you discard the thought of trading your bitcoin for fiat, you instead begin to think of the value of things relative to bitcoin and what it can buy you, such as a house, a car, groceries, etc.

In reality, what is volatile are fiat currencies. How many currencies have risen and fallen over the centuries? How consistently are they diluted and deprived of their original value? How scarce are they? We should be encouraged to begin asking these questions.

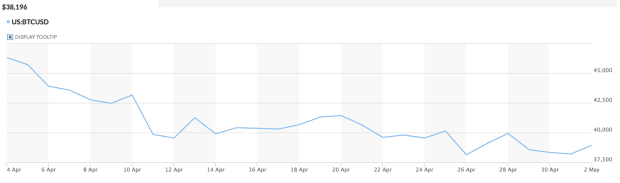

Time Preference

These questions are essentially reflected by one’s time preference: If you have a very high time preference, then you place more emphasis on the present and near-term price action. If you have a lower time preference, meaning a higher predisposition for patience and delayed gratification, then longer-term performance is more meaningful. Your time horizon will inevitably affect your perception of events.

The following image shows bitcoin’s performance over a recent one-month time period. The next image shows bitcoin’s total return since 2010. When viewed on a long enough time horizon, we can see that bitcoin doesn’t look volatile at all. In fact, it seems to be fairly consistent in its trajectory to the top-right corner.

Conclusion: There Is Nowhere Else To Put Your Money

The main emphasis of this article is to stimulate the reader’s mind into asking questions, to interrogate the apparent “normalcy” of the existing paradigm and to undertake thoughtful inquisition into the possibility of a better, more humane arrangement.

Bitcoin is founded on natural law; it is objective truth, governed by the laws of mathematics and physics. It is engineered money. Contrast this with central banks who manipulate interest rates on a whim, which typically decline decade after decade. Not only are you losing purchasing power, but you are actively being robbed.

Bitcoin not only offers security, integrity and transportability, but also offers simplicity to its users. Gone are the days of stock-picking and head-scratching — bitcoin provides the option of a simple and secure means for retaining your wealth into the future.

I challenge the reader to find a more secure, better-performing store of value for their money. Bitcoin is the hurdle to beat and the best means for securing your wealth across space and time. For those who have the fortune of reading this article now and possess courage to enter the new paradigm, they will be rewarded with an explosion in their net worth since they are entering the market at the beginning of the S-curve, taking full advantage of the adoption phase of a technology, where they can sit back and witness Metcalfe’s Law and the Lindy effect play out beautifully.

Bitcoin is the opportunity of a millennium. It is the oasis in the desert, the safe harbor in the storm, the shield against the arrows. Reclaim your sovereign birthright, return to your destiny and fear no longer.

This is a guest post by Beren Sutton-Cleaver. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.

[ad_2]

Source link